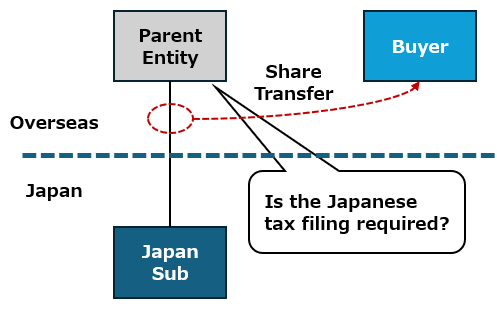

In M&A transactions or overseas group reorganizations, the shareholder of a Japanese subsidiary may change when its foreign parent company transfers the subsidiary’s shares to a third party.

Because both parties to the transfer are foreign corporations, it is often assumed that “no action is required in Japan because the transaction does not involve a Japanese company.”

However, if a foreign parent company transfers shares in a Japanese subsidiary, there are cases where the foreign parent company itself may be required to file the tax return and pay corporate tax in Japan.

If this point is overlooked, the seller may face a risk of substantial additional tax assessments in a future tax audit.

This article summarizes the key Japanese tax points that the Japanese subsidiary of a foreign-owned group should understand when its foreign parent company transfers shares in the Japanese subsidiary.

- General Rule: Capital Gains from the Transfer of Shares in a Japanese Subsidiary by a Foreign Corporation Are Not Taxable in Japan

- Exception 1: The 25/5 rules

- Exception 2: Transfer of Shares in a Real Estate Holding Corporation

- Review of Tax Treaties: Even If Taxable Under Domestic Law, the Conclusion May Change Under an Applicable Treaty

- Taxpayer Responsible for Filing

- Treatment of Local Taxes, Consumption Tax, and Withholding Tax

- How Our Office Can Support You

- Summary

General Rule: Capital Gains from the Transfer of Shares in a Japanese Subsidiary by a Foreign Corporation Are Not Taxable in Japan

Unless a foreign corporation (foreign parent company) has a permanent establishment (PE) in Japan, it is taxed in Japan only on Japan-source income.

As a general rule, capital gains from the transfer of shares are not included in Japan-source income. Therefore, even if a foreign parent company realizes a gain from the transfer of shares in a Japanese subsidiary, the gain is generally not subject to tax in Japan.

- Capital gains from the transfer of shares in a Japanese subsidiary by a foreign corporation are generally not subject to tax in Japan.

- However, this is only the general rule. It is important to note that there are significant exceptions.

If the transfer falls within certain categories described below, the gain will be treated as Japan-source income and may be subject to Japanese tax filing requirements.

Exception 1: The 25/5 rules

The most important exception to consider is a transfer that falls within the scope of a “25/5 rule”. A transfer of shares that satisfies both of the following requirements is treated as Japan-source income and is subject to Japanese taxation.

- At any time during the three-year period ending on or before the last day of the fiscal year of transfer, the transferring corporation and its specially related shareholders, etc. held 25% or more of the total issued shares of the Japanese subsidiary.

- During the fiscal year of transfer, those specially related shareholders, etc. transferred 5% or more of the total issued shares of the Japanese subsidiary.

In foreign-owned corporate groups, it is common for the foreign parent company to hold 100% (or at least a majority) of the shares in the Japanese subsidiary.

As a result, when the foreign parent company transfers shares in the Japanese subsidiary, the 25/5 requirements above will almost certainly be satisfied, and the transfer will generally fall within the scope of a 25/5 rule.

In other words, if the analysis stops at the general statement that “capital gains of foreign corporations are generally non-taxable in Japan,” a taxable transaction may be missed. In share transfers involving foreign parent-subsidiary structures, it is important to recognize that the transaction is relatively likely to be taxable in Japan.

Exception 2: Transfer of Shares in a Real Estate Holding Corporation

Another exception is the transfer of shares in a real estate holding corporation (i.e., shares in a real estate-related corporation).

If the Japanese subsidiary whose shares are transferred qualifies as a real estate-related corporation—meaning that 50% or more of the total value of its assets consists of land or similar real estate located in Japan—the gain from the transfer of those shares is treated as Japan-source income and is subject to Japanese taxation.

- Land or similar real estate located in Japan accounts for 50% or more of the Japanese subsidiary’s total assets.

- This issue is particularly relevant when transferring shares in a subsidiary that holds significant real estate, such as a real estate SPC or real estate leasing company.

When transferring shares in a Japanese subsidiary that holds significant real estate, the real estate holding corporation rules may result in Japanese taxation even if the transaction does not fall within the 25/5 rule. A separate review is therefore necessary.

Review of Tax Treaties: Even If Taxable Under Domestic Law, the Conclusion May Change Under an Applicable Treaty

The 25/5 rules and transfers of shares in real estate holding corporations are rules under Japanese domestic law.

However, when a foreign corporation is involved, it is essential to review the applicable tax treaty in addition to Japanese domestic law.

Even if the gain is taxable under Japanese domestic law, an applicable tax treaty between Japan and the country where the foreign parent company is located may limit Japan’s taxing rights, resulting in no Japanese taxation.

For example, the treatment of “25/5 rule” varies significantly depending on the treaty partner country.

Japan-U.S. Tax Treaty: Capital gains on the 25/5 rule are generally taxable only in the country of residence (the United States).

→ If the parent company is a U.S. company, the gain is not taxable in Japan.

Japan-Singapore Tax Treaty: Taxation by the source country (Japan) is permitted.

→ If the parent company is a Singapore company, Japanese taxation may arise.

As shown above, even for the 25/5 rule, whether the capital gain is subject to tax in Japan depends on the country where the foreign parent company is located.

For shares in real estate holding corporations, many tax treaties allow taxation in the country where the real estate is located (Japan), so the applicable treaty must also be reviewed carefully.

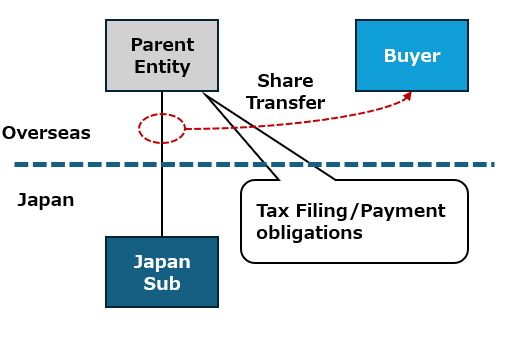

Taxpayer Responsible for Filing

If the transfer of shares in a Japanese subsidiary is taxable in Japan, the party responsible for filing and paying the tax is the foreign parent company that transferred the shares. The Japanese subsidiary itself is not the taxpayer.

That said, because a foreign parent company often has no office or personnel in Japan, it is necessary in practice to consider how to address the following matters.

- Appointment and notification of a tax agent: Appoint a tax agent in Japan (such as a person in charge at the Japanese subsidiary or the tax advisor) and submit the relevant notification to the tax office.

- Preparation and filing of a corporate tax return: Prepare and file a Japanese corporate tax return for the Japan-source income (capital gain on the share transfer), with the foreign parent company as the taxpayer.

- Management of filing deadlines: In principle, the filing deadline is within two months from the day following the end of the fiscal year in which the transfer occurred (noting the rules applicable to filing deadlines for foreign corporations).

- Preparation and submission of other required forms: Prepare and submit any required forms in addition to the tax return.

- Tax payment arrangements: Because the filing and payment obligations belong to the parent company, it is necessary to consider how a foreign parent company with no Japanese bank account or similar arrangements will make the tax payment.

The Japanese subsidiary may also need to take certain indirect actions in connection with the change in shareholder, such as filing a notification of changes and updating shareholder information in Schedule 2 of the corporate tax return (used for determining family-company status).

Treatment of Local Taxes, Consumption Tax, and Withholding Tax

For a transfer of shares in a Japanese subsidiary by a foreign parent company, it is also necessary to consider taxes other than corporate tax.

- Withholding tax: In principle, no withholding tax is required on consideration paid for the transfer of shares in a Japanese corporation (note that this differs from the treatment of consideration paid for transfers of real estate).

- Consumption tax: The transfer of shares (securities) is a non-taxable transaction for Japanese consumption tax purposes, and no consumption tax is imposed.

- Local taxes: Corporate inhabitant tax and enterprise tax are not imposed unless the foreign corporation has a permanent establishment (PE) in Japan. Therefore, for a foreign parent company without a PE in Japan, generally only national corporate tax is imposed.

How Our Office Can Support You

Japanese tax issues arising from a foreign parent company’s transfer of shares in a Japanese subsidiary require analysis under both Japanese domestic law (whether the income qualifies as Japan-source income) and the applicable tax treaty. Proceeding on an incorrect assumption—such as “this is an overseas-to-overseas transaction, so Japan is irrelevant”—can create significant risks in a future tax audit.

In addition, if a tax filing is required, the process differs from ordinary corporate tax return preparation in several respects, including preparation of the tax return and financial statements, required forms and notifications, and tax payment arrangements.

Our office supports Japanese tax filing and payment matters for foreign parent companies in these situations.

- Determination of Japanese tax implications of a foreign parent company’s transfer of shares in a Japanese subsidiary (including analysis of whether the transfer falls under the 25/5 rules or real estate holding corporation share rules).

- Review of applicable tax treaty treatment and support for preparation and submission of treaty-related forms, where applicable.

- Acting as tax agent for the foreign parent company in Japan, and preparing and filing corporate tax returns and other required forms.

- Advice on tax payment methods and related practical matters.

If you have any questions regarding Japanese tax matters in connection with a change in the parent company or share transfer involving a foreign-owned Japanese company, please feel free to contact us.

Summary

When a foreign parent company transfers shares in a Japanese subsidiary, there are cases where Japanese corporate tax filing and payment obligations may arise, even if both parties to the transaction are foreign corporations.

In particular, foreign parent-subsidiary structures often fall within the 25/5 rules, and whether Japan may tax the gain depends on the applicable tax treaty.

There are many cases where parties assume that “Japan is irrelevant because the transaction is between foreign companies,” only to find that a Japanese tax filing was actually required.

We recommend reviewing the Japanese tax implications early from both domestic law and tax treaty perspectives, taking into account the country where the foreign parent company is located, its ownership ratio, the percentage of shares transferred, and the asset composition of the Japanese subsidiary.

**********************

This article provides general information only and may include personal views. The conclusion may differ depending on the specific facts and circumstances. Before making any specific decision or taking any action based on this article, you should consult a tax professional.

Our office is available for consultations, so please feel free to contact us.

If you have questions such as “How would this apply to our company’s situation?” or “We would like to discuss a more specific case,” please feel free to contact us.

We also welcome discussions with fellow professionals, as well as spot consultations and collaboration opportunities.

The copyright in the tables and images included in this article belongs to our office. Unauthorized reproduction, duplication, or quotation is prohibited. If you wish to quote this article, please clearly indicate the source and contact us in advance.