When a foreign company establishes a subsidiary in Japan, it becomes subject to a range of national and local taxes that go well beyond corporate income tax. Many newcomers focus only on “corporate tax,” but a company incorporated in Japan may also be exposed to local inhabitant tax, enterprise tax, consumption tax, and several property-related local taxes.

Understanding the full picture from the outset helps avoid surprises in cash-flow planning and supports smooth tax compliance after incorporation. This article focuses primarily on the main taxes that commonly apply to a corporation established in Japan, such as a Japanese subsidiary, and provides a high-level explanation of how each tax is calculated.

This article is intended as a general orientation.

The tax treatment of a Japanese branch, permanent establishment, or representative office of a foreign corporation may differ from that of a Japanese subsidiary and should be reviewed separately.

In addition, tax rates and rules may vary by locality and are subject to annual tax reforms, so the figures and explanations below are illustrative.

- Types of Taxes Imposed on a Corporation

- Corporate Tax – Calculation Overview

- Local Inhabitant Tax – Calculation Overview

- Enterprise Tax – Calculation Overview

- Consumption Tax – Calculation Overview

- Business Office Tax – Calculation Overview

- Depreciable Asset Tax and Fixed Asset Tax – Calculation Overview

- Summary

Types of Taxes Imposed on a Corporation

A corporation operating in Japan is typically subject to the following taxes. The table below summarizes each tax together with its tax base, filing deadline, and where the return is filed.

As a general rule, corporate tax, local inhabitant tax, enterprise tax and consumption tax returns should be filed within two (2) months after the fiscal year-end. In some cases, one (1) month extension of the filing deadline may be available upon application; however, the payment deadline and applicable interest rules should be considered separately.

Business office tax has no such extension, and the depreciable asset tax follows a separate January calendar.

Corporate Tax – Calculation Overview

Corporate tax is a national tax imposed on a corporation’s taxable income.

Financial accounting aims at a fair measurement of periodic profit and loss, whereas the tax law aims at fairness of taxation. For this reason, taxable income is not simply the accounting net income.

Instead, it is computed by starting from the accounting profit and making tax adjustments – additions and deductions that reflect (i) items where the timing of an expense differs between accounting and tax purposes (for example, reserves and unsettled liabilities, etc.), and (ii) items that are not deductible for tax purposes (for example, a portion of entertainment expenses and certain director remuneration, etc.).

Simplified illustration (figures for example only):

The national corporate tax rate is 23.2% (a reduced 15% rate applies to small and medium-sized enterprises on the first JPY 8 million of annual income), and a local corporate tax of 10.3% of the corporate tax amount is added on top.

For fiscal years beginning on or after 1 April 2026, a new Special Corporate Tax for Defense will apply. Broadly, it is calculated at 4% of the base corporate tax amount after deducting a basic allowance of JPY 5 million. Even where the tax amount is nil, a filing obligation may still arise.

Local Inhabitant Tax – Calculation Overview

Local inhabitant tax is imposed on the corporation itself as a member of the local community. It has two components.

Corporate tax levy : calculated by multiplying the corporate tax amount by a set rate. In Tokyo the standard rate is 7% and the over-threshold (excess) rate is 10.4% for certain corporations (for example, those with capital over JPY 100 million). In Osaka, the prefectural rate is 1% (standard) / 2% (excess) and the Osaka City rate is 6% (standard) / 8.2% (excess).

Per capita levy : a fixed amount determined by the company’s capital and number of employees as below. It is imposed even if the company has no profit.

For corporations with offices exclusively within the special wards of Tokyo

Note: outside Tokyo, separate returns are filed with both the prefecture and the municipality, so the rates are set for each. Excess tax rates can differ by local government.

Enterprise Tax – Calculation Overview

Enterprise tax is a prefectural tax on a corporation’s business activities, imposed by the prefecture where the corporation has its offices. For an ordinary business company it is, like corporate tax, based on income.

For a corporation with registered capital amount over JPY 100 million, “size-based” taxation (“外形標準課税”) also applies, taxing value-added and capital in addition to income.

Income levy : a rate applied to income (roughly 1.0%–7.48%).

For companies not subject to size-based enterprise taxation, the income levy is generally applied at progressive rates based on income. For companies subject to size-based enterprise taxation, the income levy rate is lower, but value-added and capital levies are also imposed.

Value-added levy (size-based): 1.26% of value-added in Tokyo. Value-added is broadly the total of compensation and salaries, net interest paid, net rent paid, and the single-year profit or loss.

Capital levy (size-based): 0.525% of capital, etc., in Tokyo.

Separately, a Special Corporate Enterprise Tax is imposed, calculated by applying 37% (or 260% for size-based taxpayers) to the income levy at the standard rate.

From fiscal years beginning on or after 1 April 2026, the scope of size-based taxation has been broadened to capture certain large-group subsidiaries even where stated capital is JPY 100 million or less, so the JPY 100 million threshold above is a simplification.

This point is particularly relevant for foreign groups, because a Japanese subsidiary with stated capital of JPY 100 million or less may still fall within the scope of size-based enterprise taxation if it is a wholly owned subsidiary of a large group and meets the relevant paid-in capital and capital surplus thresholds.

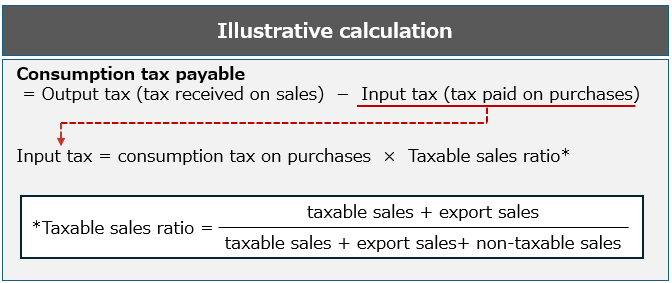

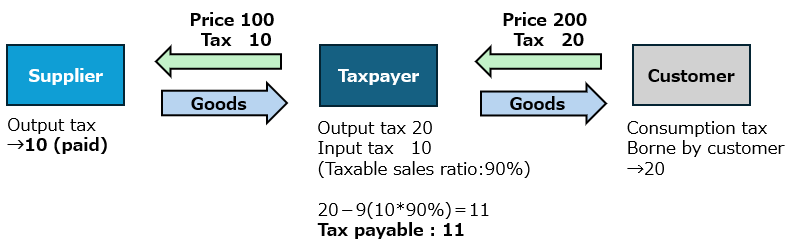

Consumption Tax – Calculation Overview

Consumption tax is an indirect tax (national plus local) on taxable transactions, with a standard rate of 10% (a reduced 8% rate applies to certain items such as food).

In simple terms, a taxpayer needs to pay the net amount between the tax it collects on sales and the tax it pays on purchases.

Taxable business enterprise (in case that taxable sales ratio is 90%) buys goods for JPY 110 (price 100 + input tax 10) and sells them to a customer for JPY 220 (price 200 + tax 20).

Taxpayer collects JPY 20 of output tax and has paid JPY 9 of input tax (input tax 10 * 90% = 9).

Thus, the tax payable should be 20 − 9 = JPY 11.

Two points often matter for new entrants: a business may qualify as a tax-exempt enterprise where taxable sales in the base period were JPY 10 million or less (though electing to be a taxable enterprise can be preferable where refunds are expected), and since October 2023 the qualified invoice (“invoice”) system affects whether input tax is creditable.

New entrants should also consider whether the company qualifies as a tax-exempt enterprise. For example, certain newly established companies may be taxable from the first fiscal year depending on their capital amount or group relationship. In addition, registration as a qualified invoice issuer generally results in the company becoming a taxable enterprise for consumption tax purposes.

Business Office Tax – Calculation Overview

Business office tax is a purpose tax imposed by designated large cities to fund the development and improvement of the urban environment. It is levied on corporations and individuals that operate offices or business establishments in those cities.

Business office tax = (i) + (ii)

(i) Office floor area × JPY 600/m² (asset levy)

(ii) Total employee salaries × 0.25% (employee levy)

In practice, exemption thresholds apply: the asset levy generally arises where total business floor area in the city exceeds 1,000 m², and the employee levy where the number of employees exceeds 100. These thresholds should be confirmed for the specific municipality.

Depreciable Asset Tax and Fixed Asset Tax – Calculation Overview

Strictly, there is no separate tax called “depreciable asset tax.”

Fixed asset tax is the tax imposed by the municipality where land, buildings, and depreciable assets are located. To distinguish it from fixed asset tax on land and buildings, the fixed asset tax on depreciable assets is, in practice, called “depreciable asset tax.”

Depreciable asset tax: assessed value of depreciable assets × 1.4%.

No tax arises where the tax base is below JPY 1.8 million. It is declared by the taxpayer: the company files a declaration of depreciable assets by 31 January, and the municipality assesses the tax.

Fixed asset tax (land and buildings): assessed value × 1.4%.

Unlike depreciable asset tax, the municipality assesses and levies the tax (it is not self-declared).

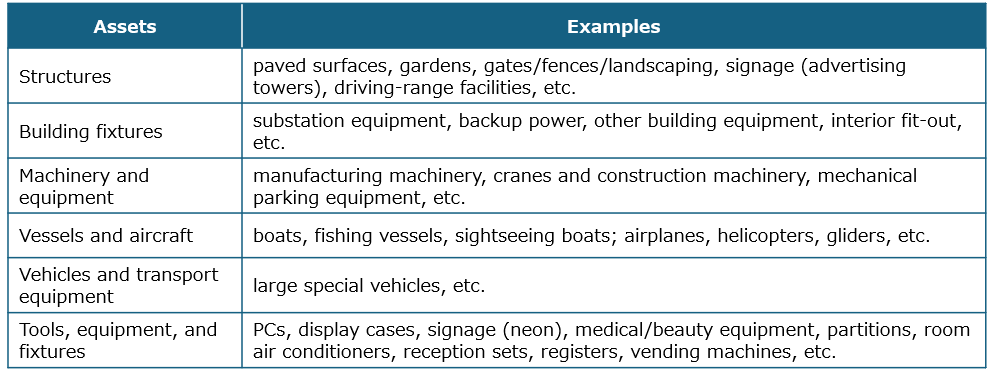

Depreciable assets are business-use assets other than land and buildings – for example:

Summary

A corporation in Japan faces not only corporate tax but a layered set of national and local taxes – inhabitant tax, enterprise tax, consumption tax, business office tax, and the property-related fixed asset and depreciable asset taxes. Each has its own tax base, rate, filing route, and calendar.

For a foreign company entering Japan, mapping these obligations early supports accurate budgeting and smooth compliance. Because rates and rules vary by locality and are revised through the annual tax reform, advice tailored to the specific situation is recommended before relying on any of the figures above.

The taxes discussed above are only a high-level overview of the main tax obligations that may arise when a company is established or operates in Japan. In practice, Japanese tax calculations can be highly complex, and the applicable treatment may vary depending on the company’s capital structure, business model, transaction flows, local jurisdiction, and whether the entity is a subsidiary, branch, or other form of presence in Japan.

Foreign companies entering the Japanese market are therefore encouraged to review their tax position at an early stage and seek professional advice tailored to their specific circumstances.

Our firm provides practical and detailed support for foreign-owned companies and multinational groups operating in Japan. If you have any questions regarding Japanese corporate tax, consumption tax, local tax filings, or tax compliance for a newly established Japanese entity, please feel free to contact us.

********************

This article is intended for general informational purposes only and does not constitute tax advice. The appropriate tax treatment may vary depending on the specific facts and circumstances. Please consult a qualified tax professional before taking any action based on this article.

Our firm also provides consultations – please feel free to contact us.

The copyright in the tables and images in this article belongs to us; unauthorized reproduction, copying, or citation is prohibited. If you wish to cite this article, please clearly indicate the source and contact us in advance.