In Japanese M&A practice, both a share deal (stock deal) and a business transfer (asset deal) are commonly used transaction structures. However, their legal and tax consequences differ significantly, so the right structure should be evaluated carefully on a deal-by-deal basis.

This article summarizes the key differences between a share deal and a business transfer, with a particular focus on Japanese tax considerations. For foreign-invested groups and multinational companies acquiring or restructuring Japanese operations, the structure selected at the outset can also affect contracts, licenses, hidden liabilities, post-deal integration, and exit flexibility.

What Is a Share Deal and What Is a Business Transfer?

Broadly speaking, the two structures work as follows:

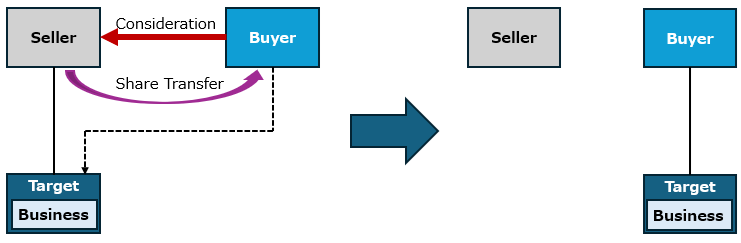

Share Deal

The seller transfers the shares of the target company to the buyer and receives consideration for the share transfer.

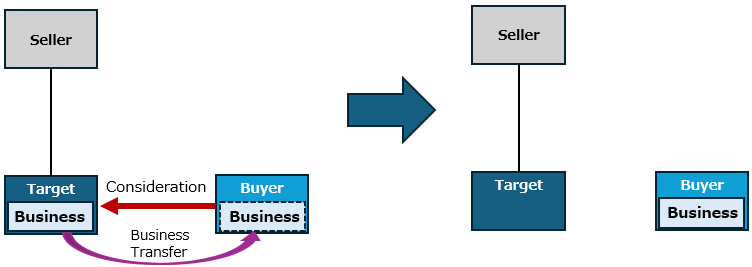

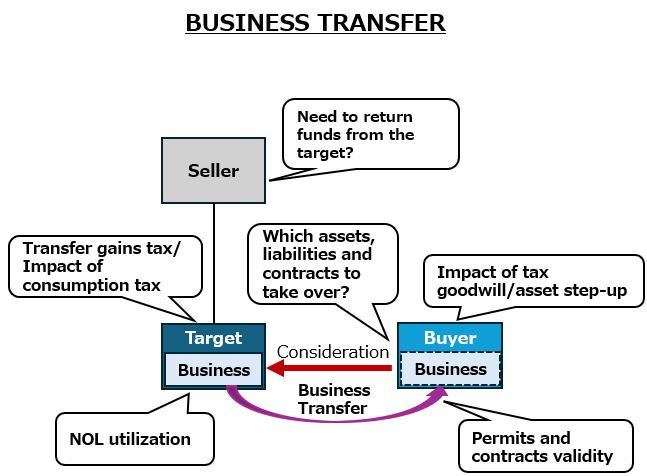

Business Transfer

The target company transfers a business to the buyer, including the assets and liabilities necessary for that business.

In a share deal, the buyer acquires the shares of the target company and, as a result, acquires the business together with the corporate entity itself. This generally means the buyer succeeds to the company as a whole, including its assets, liabilities, contracts, permits, and licenses.

By contrast, in a business transfer, the buyer acquires individual assets and liabilities held by the target company. This can make it easier to ring-fence unwanted items and avoid inheriting certain contingent exposures or off-balance-sheet liabilities that would otherwise remain inside the company in a share deal.

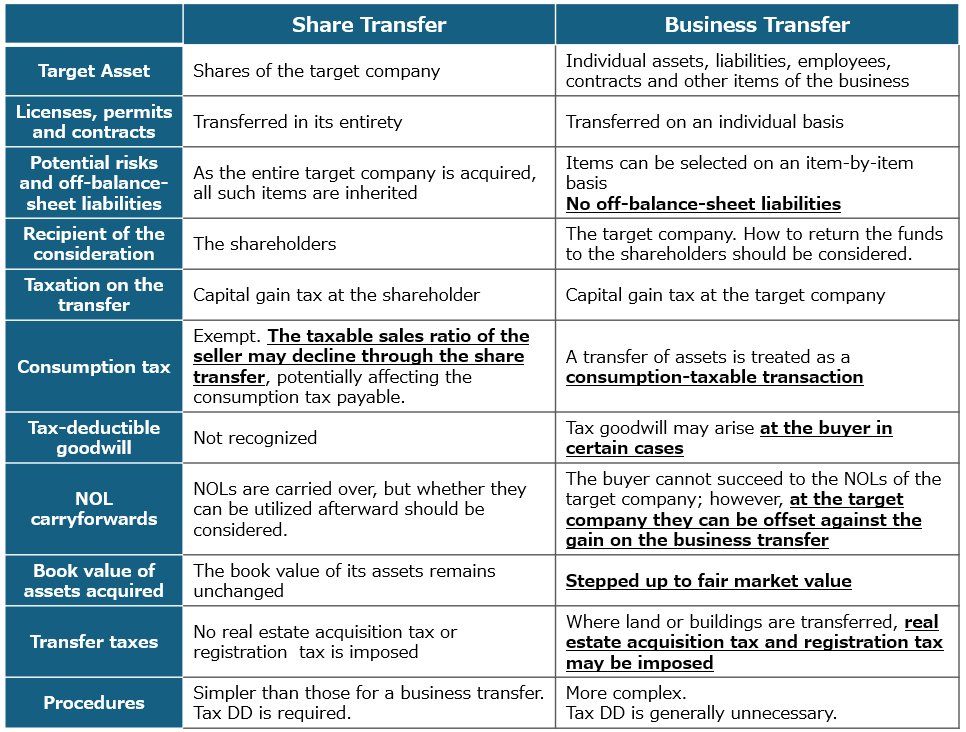

Other Key Differences

There are many additional differences between the two structures. Rather than describing every point in detail, the following comparison chart lists the main issues comprehensively:

When deciding between the two structures, the parties should not look only at the immediate tax cost of the transaction. The analysis should also take account of the specific facts, the commercial objective, and the buyer’s longer-term plan for the acquired Japanese business.

In particular, it is important to consider questions such as:

“How will the acquired company or business be operated after closing?“

“Is there a possibility of a future merger with another group company?“,

“Is a future disposal or IPO being considered?“.

For foreign-owned groups, these forward-looking issues can be just as important as the up-front tax analysis.

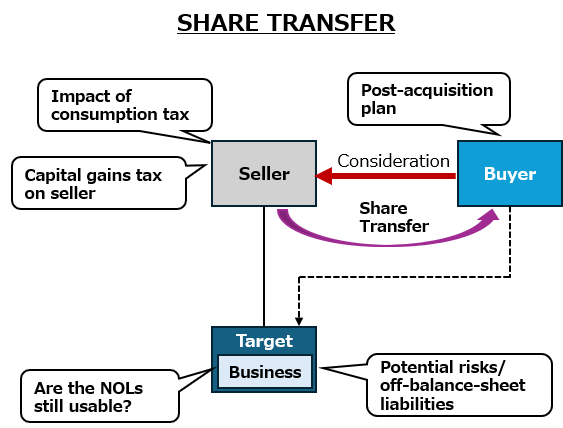

Key Practical Points to Check

Based on the above, the original article illustrates the main practical points to review when comparing a share deal and a business transfer:

As these diagrams suggest, there are numerous differences between a share deal and a business transfer. The tax impact on each party can change materially depending on which structure is selected.

The more advantageous approach depends on the specific situation. Even where one structure appears superior from the perspective of a single tax issue, the overall result may favor the other structure once non-tax considerations are taken into account as well. For that reason, it is critical to identify and prioritize the relevant issues before finalizing the transaction structure.

For foreign-invested companies, this exercise often requires combining Japanese tax analysis with practical implementation issues such as transfer of employees, assignment of contracts, treatment of permits and licenses, grouping of acquired operations into an existing Japan platform, and future repatriation or exit planning. Early structuring advice can therefore reduce both execution risk and post-closing surprises.

*******************************

This article provides only a general overview and also reflects personal views in certain respects. The appropriate conclusion may differ depending on the specific facts and circumstances of each case. Before making any concrete decision or taking any action based on this article, you should consult a qualified tax professional.

Our office would be pleased to discuss these issues with you. If you would like to understand how these points apply to your group’s Japanese operations or to a specific transaction, please feel free to contact us.

We also welcome discussions with other professionals regarding technical tax issues, second-opinion input, or project-based collaboration.

The copyright in the tables and images included in this article belong to our office. Unauthorized reproduction, duplication, or quotation is prohibited. If you wish to quote any part of this article, please clearly indicate the source and contact us in advance.