In an M&A transaction, tax due diligence (tax DD) is commonly conducted alongside financial and legal due diligence.

From a buyer’s perspective, however, it is not always clear why tax DD is necessary, or what the buyer actually gains by spending time and money on it. In practice, tax DD is sometimes treated as just another procedural step. In some transactions, only financial DD is performed, and tax DD is omitted altogether.

Tax DD, however, is not merely an add-on to financial DD. It is a process that directly affects the buyer’s core investment decisions: whether to buy, how to buy, and at what price.

The author has been involved in a wide range of M&A tax DD engagements at a big4 tax firm, including transactions worth several billion JPY, large-scale transactions in the tens or hundreds of billions of JPY, and cross-border transactions involving numerous target companies in Japan and overseas.

Drawing on that experience, this article explains, from the buyer’s perspective, why tax DD should be performed and what it is intended to achieve.

The Three Main Reasons for Tax DD

Why is tax DD necessary?

Broadly speaking, the reasons can be grouped into the following three categories:

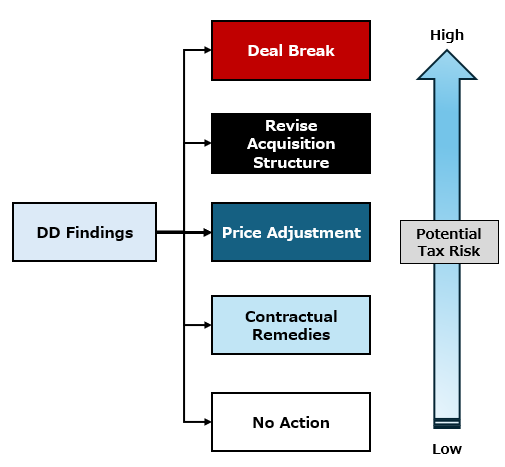

- Understanding potential tax risks — should the buyer acquire the target at all?

- Identifying the appropriate acquisition structure — is a simple stock deal really the best structure?

- Identifying items to be reflected in the purchase price and the SPA, including representations, warranties and indemnities

The starting point of tax DD is to understand the potential tax exposures that the target company may carry.

If the target has made errors in past tax filings, or has taken tax positions that are open to different interpretations, the buyer may effectively bear the risk of additional tax assessments after closing. This is why it is important to identify the nature and potential amount of such risks before signing or closing the transaction.

Next, based on the risks identified and the target’s overall tax profile, the buyer considers the appropriate acquisition structure. If significant tax exposures are identified, is acquiring the shares of that company really the right approach? Choosing an asset deal or a corporate split instead of a share acquisition may materially affect whether historic tax risks can be ring-fenced, as well as the tax efficiency of the transaction after closing.

Finally, the buyer considers whether the identified risks should be reflected in the purchase price, or addressed through representations, warranties, indemnities or closing conditions in the SPA.

In other words, the purpose of tax DD is not the investigation itself. Its purpose is to translate the findings into concrete actions — price negotiation, deal structuring and contractual protections. This is the key reason why a buyer conducts tax DD.

Financial DD typically focuses on matters such as the target’s earnings capacity, working capital, net debt and normalized earnings. However, issues such as past tax filing errors, the usability of tax loss carryforwards, the tax treatment of past reorganizations, and transfer pricing exposures may not be fully identified without review by tax specialists.

What Tax DD Examines and Why It Matters

Tax DD covers a range of tax-related issues. The main areas are set out below, with a focus on why each item is reviewed and what it means for the buyer.

- The target’s tax positions

- Tax loss carryforwards / net operating losses (NOLs)

- Tax audit history

- Past reorganizations

- Related-party transactions

- Unusual or non-recurring transactions

- Tax compliance status/profile

1. Tax Positions

A target company’s tax treatment may include positions that are open to interpretation, or positions deliberately taken on uncertain tax issues. In some cases, past tax treatment may simply be incorrect.

If the tax authorities later challenge such positions, additional taxes, penalties and interest may arise. Where the buyer acquires the shares of the target company, the buyer effectively inherits these potential exposures. It is therefore essential to understand what tax positions have been taken, the basis for those positions, and the potential financial impact if they are identified at the tax audit.

It is also important to understand the target’s overall tax profile. For example, is the target generating taxable income, or does it have tax losses? If it is generating taxable income, how much tax does it pay each year?

Accounting profit and taxable income can differ significantly. A company may be loss-making for accounting purposes but still pay substantial tax, or it may be profitable in its financial statements while being in a tax loss position. These differences may not be apparent from the financial statements alone, which makes an accurate understanding of the target’s tax position particularly important for the buyer.

2. Tax Loss Carryforwards / Net Operating Losses

Whether the target has tax loss carryforwards (NOLs) directly affects its future tax payments, cash flows, valuation, purchase price and the buyer’s financial model.

However, the fact that NOLs are shown on the target’s tax returns does not necessarily mean that they can be used after the acquisition. The buyer should confirm not only whether such NOLs exist, but also how long they remain available, why they arose, and whether the amounts recognized as tax losses are valid from a tax perspective.

In one tax DD engagement, the target recognized NOLs on its tax returns, but because of a past reorganization, some of those losses should not have been available for use. This issue was identified through tax DD.

It is also critical to consider whether the acquisition itself may trigger limitation rule on the use of NOLs after closing. In short, the key question is not only how much NOLs exist and when it expires, but whether the buyer can actually benefit from it after the transaction.

3. Tax Audit History

Tax DD also involves reviewing past tax audits, including what issues were raised by the tax authorities and how those issues were resolved.

If past audit findings were not properly addressed, the same issues may arise again in the future. Conversely, if the target has not been subject to a tax audit for a long period, there may be latent tax exposures that have not yet been challenged by the tax authorities.

Where a particular transaction appears to involve potential tax issues, it is also important to identify the fiscal year in which the transaction occurred and whether the period during which the tax authorities may reassess or make corrections remains open. This helps the buyer assess the residual tax risk.

4. Past Reorganizations

If the target has conducted mergers, company splits, share exchanges or other reorganizations in the past, the buyer should review whether each transaction was treated as tax qualified or non-tax qualified, whether that treatment was appropriate, and whether matters such as the carryover or restriction of NOLs and built-in loss limitations were properly addressed.

Japan’s reorganization tax rules are complex and can easily give rise to errors in practice. Mistakes in past reorganizations may result in future tax assessments or unexpected tax costs. Particular care is therefore required in reviewing this area.

In our experience, issues relating to past reorganizations are one of the most common sources of significant findings in tax DD. This is especially the case where the applicable tax rules were not sufficiently considered at the time of the transaction.

5. Related-Party Transactions

For transactions among group companies, particularly transactions with overseas affiliates, the buyer should review how prices are set, whether they are consistent with the arm’s length principle, and whether transfer pricing benchmarking or other supporting analysis has been prepared.

For international groups, transfer pricing adjustments can have a significant monetary impact and may become a key tax issue. In practice, it is not uncommon to find cross-border related-party transactions for which no transfer pricing analysis has been performed.

The buyer should also consider what remedial actions may be needed at or after closing, including the preparation of documentation, revision of pricing policies, or adjustment of intercompany arrangements.

6. Unusual or Non-Recurring Transactions

Transactions outside the ordinary course of business often involve complex tax treatment and can be a frequent source of tax issues.

Examples include sales of real estate or securities, debt waivers, transactions with directors or shareholders, reorganizations, share buybacks, debt-equity swaps and contributions in kind.

Tax DD reviews whether such transactions occurred in the past and, if so, whether they were treated appropriately for tax purposes. In practice, tax issues are often identified in connection with these types of unusual or non-recurring transactions.

7. Tax Compliance Status/profile

Tax DD also reviews the target’s tax compliance status, including whether tax returns have been filed on time, taxes have been paid properly, and required notifications or applications have been submitted.

These may appear to be basic items, but compliance failures can lead to unexpected tax exposures or lost tax benefits. Reviewing how tax returns are prepared and reviewed internally, and how external tax advisers or tax accountants are involved, can also help assess the target’s tax governance and compliance-related risks.

Tax DD analyzes the target’s tax risks and tax profile from many angles. For example, if an error in a past reorganization is identified and an unexpected NOL limitation rule is discovered, the buyer may not be able to achieve the post-deal tax savings originally assumed.

If such an issue is identified before closing, the buyer may be able to revisit the purchase price or adjust the acquisition structure, thereby avoiding unexpected losses after the transaction.

In Summary

The reason for conducting tax DD is to analyze tax risks and reflect the results in concrete decisions: whether to acquire the target, what structure to use, and what contractual protections should be included.

When a buyer understands why tax DD is being performed, it ceases to be a mere formality and becomes a practical tool for investment decision-making and risk management.

This is particularly important in transactions involving cross-border dealings or past reorganizations, where the issues can be complex and the quality of tax DD may have a significant impact on the post-closing tax burden. If you are considering an acquisition, it is advisable to incorporate the tax perspective as early as possible.

At our firm, a tax professional with hands-on experience in numerous M&A tax DD and structuring engagements directly supports clients from a tax perspective.

We provide flexible support regardless of deal size, tailored to the nature of the transaction and the target’s circumstances. We can assist from the early stages of considering an acquisition, around the basic agreement stage, or when determining whether tax DD should be performed. Please feel free to contact us if you would like to discuss tax DD, M&A tax matters or corporate reorganizations.

********************

This article provides a general overview and includes certain personal interpretations.

The appropriate conclusion may differ depending on each client’s specific circumstances. Before taking any concrete actions or making decisions based on the contents of this article, professional tax advice should be obtained.

Our firm is available to provide consultations, so please feel free to contact us at any time.

All tables and images included in this article are the intellectual property of our office. Unauthorized reproduction, copying, or quotation is strictly prohibited.

If you wish to quote any part of this article, please ensure that the source is clearly indicated and contact us in advance.