Japan’s Corporate Tax Law defines several types of entities as “corporations,” each with distinct legal and tax implications. For international clients doing business in Japan or considering incorporation, understanding these categories is essential for compliance, planning, and communication with Japanese tax authorities.

Domestic vs. Foreign Corporations

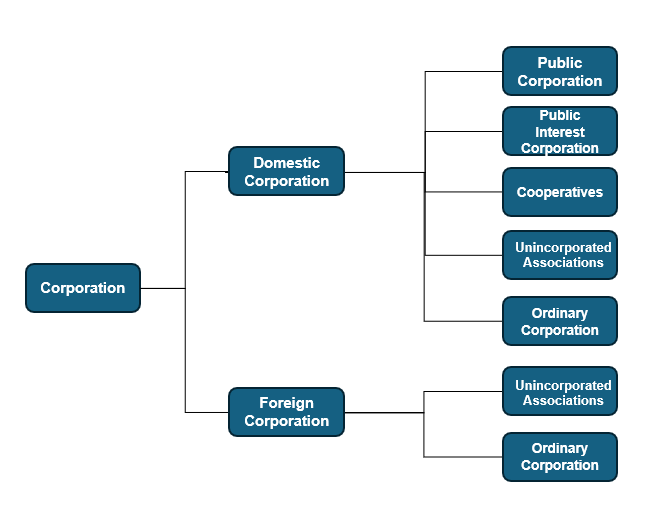

Under Japanese tax law, corporations are broadly divided into two groups:

- Domestic Corporations (内国法人): Entities with their head office or principal office located in Japan. These are subject to Japanese corporate tax on worldwide income.

- Foreign Corporations (外国法人): Entities whose head office is outside Japan. Japan applies a source‑based taxation principle. If a foreign corporation has a Permanent Establishment (PE) in Japan, only the income attributable to that PE is subject to Japanese corporate tax.

Subcategories of Domestic Corporations

Domestic corporations are further classified into five subtypes:

Foreign corporations may also be classified as ordinary corporations or unincorporated associations, depending on their structure and activities in Japan.

Common Entity Types for Business in Japan

In practice, most businesses operating in Japan adopt one of two standard corporate forms:

- Kabushiki Kaisha (KK): A joint-stock company widely used for both domestic and foreign-owned enterprises.

- Godo Kaisha (GK): A flexible, LLC-style entity suitable for small and medium-sized businesses.

These are categorized as ordinary corporations under Japanese tax law and provide clear governance structures, legal personality, and access to Japan’s corporate infrastructure.

Why This Matters for International Clients

Understanding these classifications helps foreign investors and partners:

- Select the appropriate entity type for incorporation

- Anticipate tax obligations and filing requirements

- Communicate effectively with Japanese advisors and regulators

Whether you are establishing a subsidiary, entering a joint venture, or reviewing contracts, clarity on corporate status under Japanese tax law provides a solid foundation for strategic decision-making.

*******************************************

This article provides a general overview and includes certain personal interpretations.

The appropriate conclusion may differ depending on each client’s specific circumstances. Before taking any concrete actions or making decisions based on the contents of this article, professional tax advice should be obtained.

Our firm is available to provide consultations, so please feel free to contact us at any time.

All tables and images included in this article are the intellectual property of our office. Unauthorized reproduction, copying, or quotation is strictly prohibited.

If you wish to quote any part of this article, please ensure that the source is clearly indicated and contact us in advance.